Founder's Perspectives

Founder's Perspectives

On chokepoints, legacy fragility, and the structural risk that no investment strategy actually addresses.

The Strait of Hormuz is 33 kilometres wide at its narrowest navigable point. That is roughly the distance between Mumbai’s Bandra and Thane. And yet, on any given day, nearly one-fifth of the world’s entire crude oil supply moves through that single corridor, from the Persian Gulf refineries of Saudi Arabia, the UAE, Kuwait, Iraq, and Iran out into the global economy. When tension rises in that region, which it does with some regularity, markets respond within hours. Crude prices spike. Shipping insurance costs climb. Currencies shift. Geopolitical nerves, already taut, draw tighter.

The anxiety is not about the specific conflict at hand. The anxiety is about what the conflict reveals: that the global economy, for all its sophistication and redundancy and institutional architecture, has allowed an enormous proportion of its energy flow to pass through a single narrow passage. Strategists call this a chokepoint. The more clinical term is a single point of failure. What it means in practice is that when this one corridor is threatened, there is no seamless alternative. The system freezes.

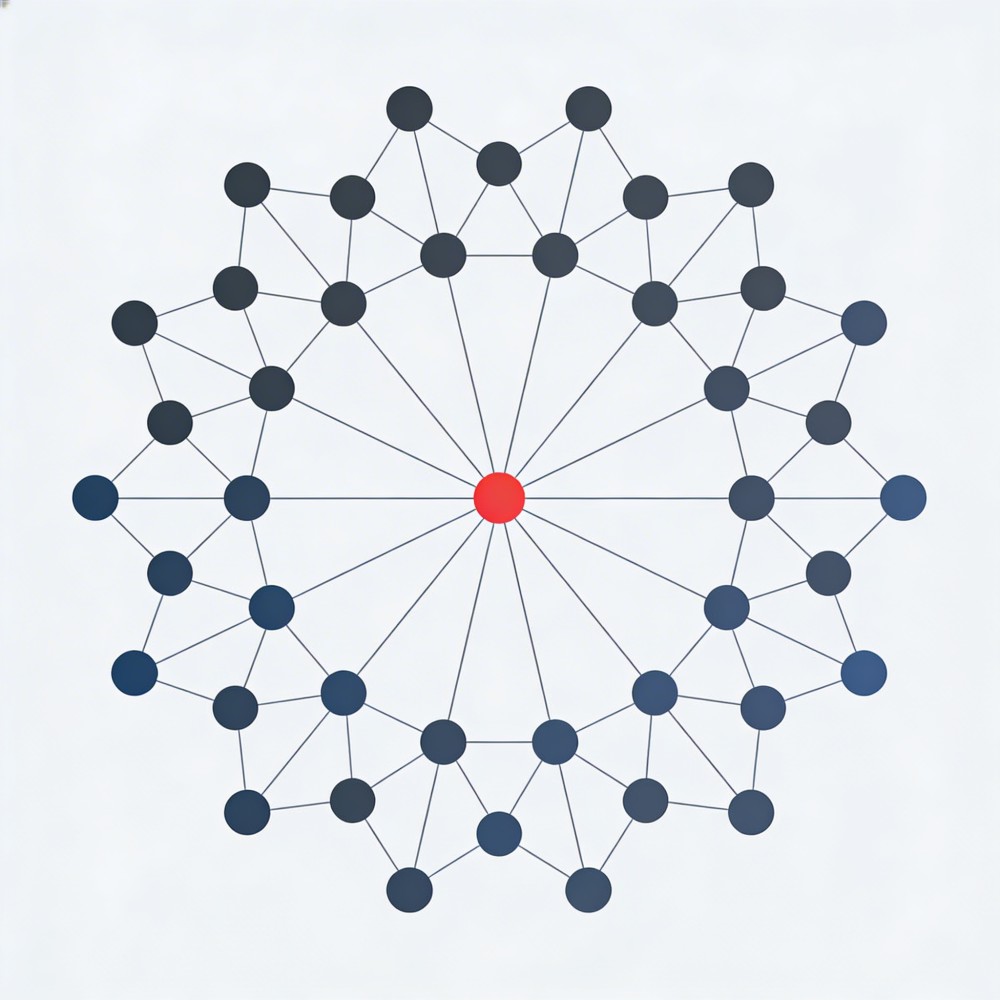

I have spent thirty years sitting with families who have built extraordinary wealth. And the pattern I keep encountering, quietly, persistently, across families of very different sizes and structures and industries, is that most of them have built their own version of the Strait of Hormuz inside their legacy architecture. They have allowed an extraordinary proportion of everything that matters, decisions, relationships, institutional knowledge, wealth itself, to flow through a single, narrow passage. And like the global economy, they remain comfortable with this arrangement right up to the moment they are not.

The chokepoint is almost never recognised as one until something forces the recognition. In the meantime, it is simply the way the family works. The patriarch makes the investment calls because he has always made them and because his track record justifies the trust. The wealth sits predominantly in the operating business because that is where it was created and where it continues to compound. The relationships with bankers, advisors, and legal counsel exist in one person’s phone and in one person’s memory, because centralising those relationships is efficient and because it reflects the natural hierarchy of how the family is organised.

Each of these arrangements makes complete sense in isolation. The patriarch’s judgment is genuinely superior. The operating business really is the best-performing asset the family owns. Centralised relationships really do produce faster, more coherent decisions. The fragility is not in any individual choice. The fragility is in the cumulative architecture that results when all of these reasonable choices point in the same direction: everything of consequence flows through one channel.

The first choke point, and the most common one I encounter, is the founder himself. In Indian family businesses, this takes a particular form that is worth naming carefully, because it is not simply a management problem. It is a cultural one. The concentration of decision-making authority in the patriarch reflects genuine respect, genuine hierarchy, and in many cases genuinely superior capability. The founder built the business. He understands it at a depth that no one else in the family has yet developed. His instincts have been tested over decades in ways that the next generation’s instincts have not. The deference he receives is not irrational.

But deference, practiced long enough, produces a particular kind of institutional blindness. The people around the patriarch stop developing their own judgment because their judgment is rarely the one that matters. The next generation learns to execute rather than to decide. The organisation learns to wait. And the founder, whose capability is real, gradually becomes the only person in the room who knows how the whole system actually works. When he steps back, by choice, by illness, or simply by the passage of time, the vacuum is not a management gap. It is an architectural one. And architectural gaps are not filled by promoting someone or hiring someone. They take years to rebuild.

The second choke point, is wealth concentration. Many of the families I work with have built the overwhelming majority of their net worth inside a single operating business, sometimes 70, 80, 90 percent of everything they own. This is entirely understandable. The business is what they know. It is what produced the wealth in the first place. Diversifying away from it can feel like a vote of no confidence in the very engine of their success. And in the compounding years, when the business is growing well and the portfolio outside it is modest by comparison, the concentration does not feel like risk. It feels like conviction.

What it actually is, structurally, is a single point of failure. A regulatory shift, a technology disruption, a market cycle turning against the sector, a key relationship souring, any one of these, in a sufficiently concentrated balance sheet, can create a liquidity problem that spreads quickly from the business into the family. I have watched families who were genuinely wealthy for decades encounter this kind of stress, and the discovery is almost always experienced as a surprise, which tells you something about how poorly we account for concentration risk when things are going well.

The third chokepoint is the one I find most underestimated, perhaps because it is the least visible. It is the concentration of institutional knowledge in a single person. In many family offices and family businesses, one individual holds the entirety of the operating intelligence: which banker to call for what, what the legal structures actually say and why they were designed that way, what the advisory relationships are and how they work, what the portfolio looks like beneath the surface-level reporting. This knowledge exists in one mind, maintained there through decades of accumulated experience, and shared with almost no one because there has never been a pressing reason to share it.

When that person is unavailable, through illness, through travel, through the simple act of sleeping, the organisation slows. When that person is gone permanently, the organisation discovers that it has been operating with institutional memory it did not know it was entirely dependent on. The knowledge was never written down because it never needed to be. The relationships were never transferred because there was no urgency. And now there is urgency, and the knowledge is gone.

The response to chokepoint risk in global energy systems is instructive. Nations build strategic reserves, stockpiles that buy time when the primary flow is disrupted. They develop alternate pipelines and shipping routes, accepting the inefficiency of redundancy because they understand that redundancy in critical systems is not waste; it is insurance. They invest in energy transition strategies that, over the long term, reduce dependency on any single geography or fuel source. The goal is not to eliminate the primary route. It is to ensure that the primary route is not also the only route.

The equivalent logic in family wealth governance is straightforward, though executing it requires a kind of discipline that feels unnecessary until it is urgently necessary. Decision-making authority needs to be distributed across investment committees, family councils, and structured advisory relationships, not because the patriarch’s judgment is no longer trusted, but because institutional intelligence is more durable than individual intelligence, and the goal is durability. Wealth needs to flow through multiple engines, operating business, financial portfolio, global assets, private investments, so that no single disruption can threaten the whole. Institutional knowledge needs to be documented, transferred, and actively shared, not because efficiency demands it today, but because continuity will demand it eventually.

And the next generation needs to be prepared in a way that goes beyond financial literacy courses and internships, important as those are. They need actual exposure to decision-making, real decisions with real stakes, while the founder is still present and available to catch the mistakes. That preparation, begun early and structured deliberately, is what converts the next generation from executors of the patriarch’s will into genuine stewards of the family’s future. The difference between those two things is the difference between a family that survives a transition and a family that does not.

When I think about what Wise Wealth actually means in practice, beyond the philosophy, beyond the language of stewardship and long-horizon thinking, I keep returning to this. Resilience is the goal. Not maximum return. Not optimal structure in any given moment. Resilience: the capacity to absorb disruption in one part of the system without the whole system failing. And resilience, by definition, cannot be built around a single point of failure.

The Strait of Hormuz is not going anywhere. The global economy will continue to depend on it because rerouting that dependency is genuinely difficult and genuinely expensive, and the urgency to do so tends to diminish when the passage is open. Families are not constrained in the same way. The chokepoints in most family wealth systems are not structural inevitabilities. They are habits, compounded over time, that nobody has yet had sufficient reason to examine.

The question worth asking before a crisis makes it urgent: where is your family’s Hormuz? Is it a person? Is it an asset? Is it a decision structure that has never been written down because it has never needed to be? Is it a relationship that exists in one person’s phone and nowhere else?

Because legacy is not most often destroyed by bad investments or market downturns. It is most often undermined by the structural fragility that accumulates, quietly and invisibly, while everything is still working exactly as it always has.

Executive Summary The RBI has introduced a temporary package aimed at attracting foreign currency inflows from Non-Resident Indians (NRIs). The measures make eligible Foreign Currency Non-Resident (Bank) [FCNR(B)] deposits significantly more attractive by enabling banks to offer higher deposit rates while also providing additional flexibility for structured financing solutions. The special window is available for […]

Every client family I sit across from this year is asking a version of the same question, in different words: where is the ground? For over a decade, our conversations with you have started from valuation, from cycles, from the reasonable expectation that patience gets rewarded. This year, I want to start somewhere more honest […]

Abuse often remains hidden in plain sight. Behind closed doors, in workplaces, within families, and across communities, countless women and children endure physical, emotional, psychological, sexual, and financial abuse without knowing where to turn for help. For many survivors, the greatest challenge is not just escaping the abuse, but finding someone who will listen without […]

signup for updates